What Is An Income Statement?

The Income Statement measures the success of a company’s operations; it provides investors and creditors with information needed to determine the enterprise’s profitability and creditworthiness. A company has earned net income when its total revenues exceed its total expenses. A company has a net loss when total expenses exceed total revenues.

A company can obtain resources through its own operations. The Income Statement presents the results of operations of a business over a specified period of time (e.g., one year, one quarter, one month) and

is composed of Revenues, Expenses and Net Income.

Revenue: Revenue is a source of income that normally arises from the sale of goods or services and is recorded when it is earned. For example, when a retailer of roller blades makes a sale, the sale would be considered revenue.

Expenses: Expenses are the costs incurred by a business over a specified period of time to generate the revenues earned during that same period of time. For example, in order for a manufacturing company to sell a product, it must buy the materials it needs to make the product.

In addition, that same company must pay people to both make and sell the product. The company must also pay salaries to the individuals who operate the business. These are all types of expenses that a company can incur during the normal operations of the business.

When a company incurs an expense outside of its normal operations, it is considered a loss. Losses are expenses incurred as a result of one-time or incidental transactions. The destruction of office equipment in a fire, for example, would be a loss.

Assets and expenses

Incurring expenses and acquiring assets both involve the use of economic resources (i.e., cash or debt). So, when is a purchase considered an asset and when is it considered an expense?

Assets vs. expenses: A purchase is considered an asset if it provides future economic benefit to the company, while expenses only relate to the current period. For example, monthly salaries paid to employees for services they already provided to the company would be considered expenses.

On the other hand, the purchase of a piece of manufacturing equipment would be classified as an asset, as it will probably be used to manufacture a product for more than one accounting period.

Net income:The Revenue a company earns, less its Expenses over a specified period of time, equals its Net Income. A positive Net Income number indicates a profit, while a negative Net Income number indicates that a company suffered a loss (called a “net loss”).

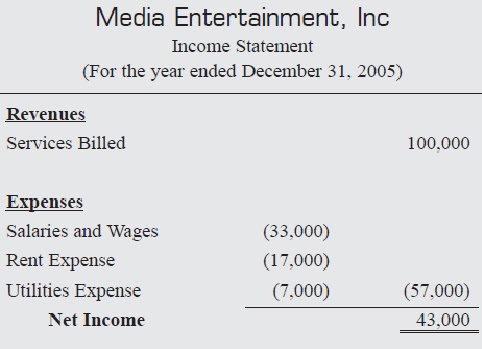

Here is an example of an Income Statement:

No comments:

Post a Comment